Compare today's top mortgage rates

Looking for a great mortgage rate? Check out the lowest mortgage rates available

March 2nd 2020

We prepare for the worst every day: We carry umbrellas when it’s cloudy, pop Gravols before a long flight, and buy travel insurance when going overseas. Why should taking on a mortgage be any different? A mortgage stress test is one way of preparing for the worst… it’s also a legal requirement in Canada.

In finance, planning for a worst-case scenario is called a stress test. It involves modelling a bad scenario before an investment is made. An example might involve starting a retirement fund with an RRSP: While an annual return of 5% might be a reasonable expectation, what if your investments only make 4% each year? Will you still have enough money to retire at 60? If not, that RRSP has failed the stress test. You can use this information to make better investments and avoid costly mistakes.

A mortgage stress test is a way of determining exactly how much you can afford (and under what circumstances). If your income was reduced or you lost your job, could you still afford to make mortgage payments? What if interest rates spike or you need to refinance your home?

This type of rainy-day planning is important for a few reasons. First, interest rates fluctuate. So do home prices. According to the Canadian Real Estate Association, Canada’s average home price was over $500,000 in January 2020, up 11% from a year before. Knowing you can still afford to pay your mortgage if interest rates increase is important, and could affect the kind of home you decide to buy.

Looking for a great mortgage rate? Check out the lowest mortgage rates available

Since 2018, all Canadian homebuyers getting a high-ratio or uninsured mortgage have been subject to a mortgage stress test. The mortgage stress test requires banks to check that a borrower can still make their payment at a rate that’s higher than they actually pay. From 6th April 2020, the way this higher interest rate is calculated will/has changed.

Here’s how it works. When you apply for a mortgage (including joint mortgages), you’ll be offered a contracted rate – hopefully this will be as low as possible! However, you bank needs to check you’ll be able to pay back your mortgage, even if your mortgage rate rises during your mortgage term. To do this, they check your ability to make your payments with one of two rates:

Generally, you’ll need to qualify for the higher of the two rates. This means that your income needs to be high enough, and your existing debt low enough, to be able to pay down your mortgage at that higher rate. Generally, this will result in you being able to borrow a smaller amount of money.

*A high-ratio mortgage is one with a down payment of less than 20% on the purchase price of a home. An uninsured mortgage is one with a down payment of at least 20%. Before 2018, only high-ratio mortgages were subject to the Canadian mortgage stress test.

Let’s have a look at an example of the mortgage stress test. Let’s say the best mortgage rate in Canada is 2.89% and the Bank of Canada’s qualifying rate is 5.19%. Assuming you qualify for the lowest rates, the two rates your mortgage stress test will use are:

According to our mortgage affordbility calculator, a family with an annual income of $100,000 with a 10% down payment and 5-year fixed mortgage rate of 2.89% amortized over 25 years would have qualified for a home valued at $511,424 under a 5.19% qualifying rate.

The change to the mortgage stress test in April 2020 has to do with how the Bank of Canada qualifying rate is calculated. Remember, the higher this rate is, the less you’ll be able to borrow, even if you get a lower mortgage rate offer.

Under the old rules, the Bank of Canada qualifying rate was set at the average of the big bank’s 5-year fixed posted rates. Effective 6th April 2020, the qualifying rate will be set at the average 5-year fixed rate for mortgages applying for default insurance on applications received by CMHC in the past week.

This adjustment means the way the mortgage stress test is calculated for both insured mortgages and uninsured mortgages will be very similar (uninsured mortgages were already stress tested at 2% higher than the rate of a mortgage). Put simply, Canadians will be stress tested at a rate that is about 2% higher than the mortgage rate they are receiving.

We think this means the stress test will drop to about 4.89% once the change takes effect on 6th April 2020, assuming current market rates. Canadians who are getting insured and insurable mortgages can expect to qualify for a little bit more than what they can today. If you can’t currently qualify for what they want, but are close, you should redo your qualifying calculations using the new stress test.

Looking for a great mortgage rate? Check out the lowest mortgage rates available

So, changes to the mortgage stress test aside, how do you figure out what minimum monthly payment you’re required to be able to afford? Here’s what you need to know.

It’s one thing to compare the best mortgage rates on our site today, but you should also assume that mortgage rates could go up in the future. If you have a variable-rate mortgage, which is attached to prime rate, this will immediately affect your mortgage payment. On the other hand, if you have a fixed-rate mortgage, you’ll keep your current low rate for the duration of your term, but will be faced with an increase once your mortgage comes up for renewal.

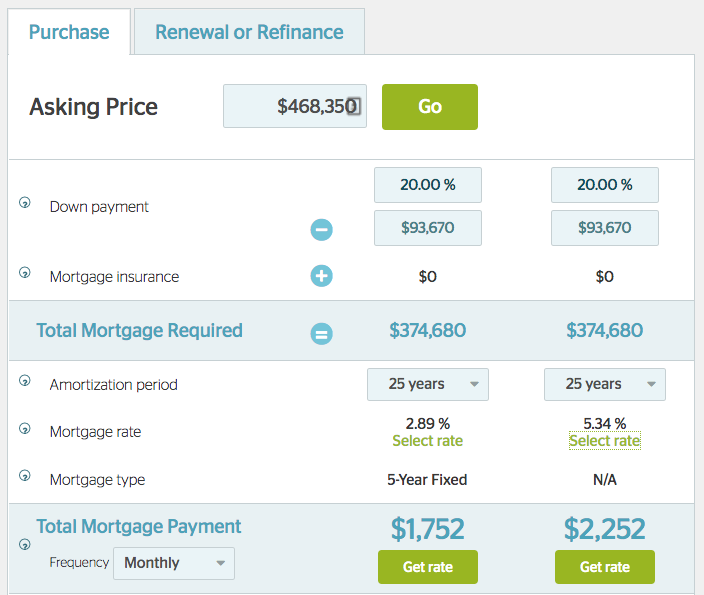

While it’s impossible to predict exactly where interest rates will be in a few years, an increase of two to three percentage points isn’t out of the question. For example, if you buy a home for $468,350, put down 20% and qualify for a five-year fixed-rate mortgage of 2.89%, you’ll have a monthly mortgage payment of $1,752. That doesn’t sound so bad.

But what if mortgage rates increase to 5.34% after your five-year term ends? According to our mortgage payment calculator, your monthly payment would rise to $2,252. Can you afford that rate today? You will have to be able to – even if you aren’t required to pay that rate – due to Canada’s mortgage stress test.

If you couldn’t afford those payments, you may need to weigh your options. Do you save a larger down payment and defer the purchase of your home? Do you choose a more affordable home? Only you know the correct choice. It’s a good idea to speak with your mortgage broker to help you figure out your best course of action.

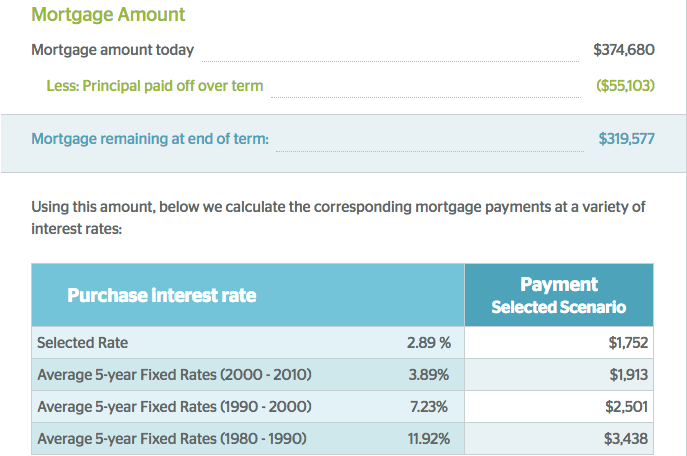

Below our calculator, we built in an Interest Rate Risk section. This shows you what the balance of your mortgage will be after this mortgage term. It then gives you some examples of what your new monthly mortgage payment could be with a variety of different rates, based on historical averages. While you probably don’t need to worry about mortgage rates ever hitting double digits again, it’s still good to be informed.

To run multiple scenarios on our mortgage payment calculator, you can also manually enter custom mortgage rates. Compare these results to your monthly budget before you buy a home that may be too expensive in the future. If you want to get serious about it, keep a spreadsheet with all the results so you can reference it later.

It’s important to keep up to date on changes to Canadian mortgage regulations, as they can directly impact your mortgage. Beyond that, the best thing you can do to increase the amount you can borrow is to earn more money (easier said that done) and save more money for a down payment.

It also doesn’t hurt to ask a mortgage broker for help when stress testing a mortgage before you buy. In addition to helping you find out what your ideal debt service ratios and maximum interest rate are, they can keep you up to date on changes to lending policies that can affect how much you can borrow.